Over the past six weeks, investors have pulled roughly $5.94 billion from US spot Bitcoin ETFs, marking the longest unbroken run of weekly outflows since these funds first opened for business in 2024. Galaxy Research puts the worst 30-day stretch at $6.35 billion through June 20.

Bitcoin has been sliding right alongside those redemptions, and after a hot inflation print on Thursday, it dropped to a 21-month low near $58,000 before steadying around $59,000, which leaves it roughly 53% below the $126,080 record it set last October.

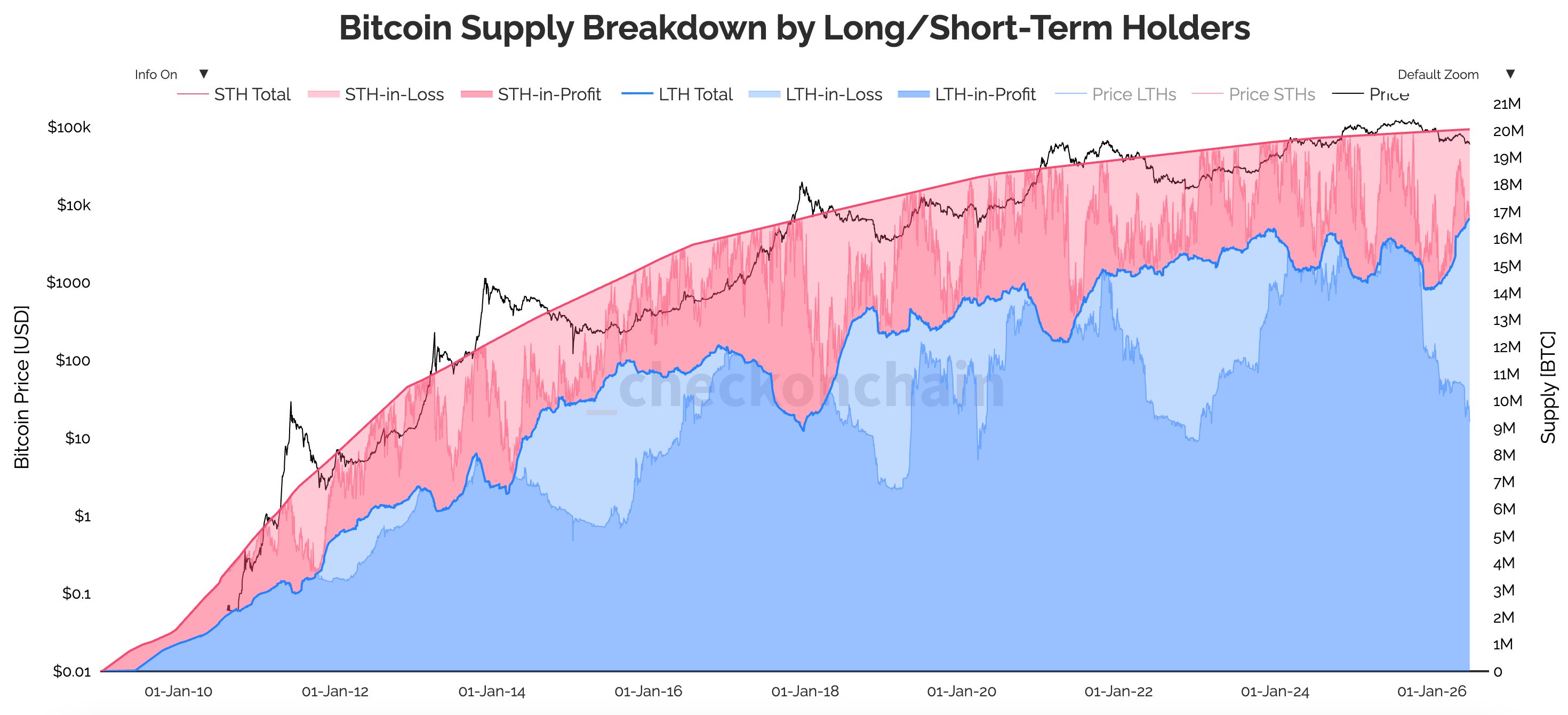

Despite the enormous outflows, the thing to pay attention to isn't the selling itself, but who's actually doing the selling. While the ETF crowd has been heading for the exits, the people who've held Bitcoin for years have barely budged: long-term holders, meaning anyone who's held for 155 days or more, own 16.64 million BTC, which amounts to close to 83% of everything in circulation.

So the supply is steadily piling up with the folks who've lived through drawdowns like this before, while the selling is coming almost entirely from allocators who showed up through a brokerage account. This is the first real capitulation for ETF holders, because it's the first time the wrapper that finally carried Wall Street into Bitcoin has shown it's losing its nerve.

The $6 billion ETF exit and who's actually leaving

If you watch how the money left, the pace tells you almost as much as the total does. The first week of June was particularly brutal, with $1.72 billion walking out the door, but by the week ending June 18, that had shrunk to just $226.8 million, a slowdown of nearly 87% in a few weeks.

Jeff Ko, the chief analyst at CoinEx, said the deceleration was a sign the selling wave is wearing itself out rather than building, with the worst of the pressure probably already behind the market.

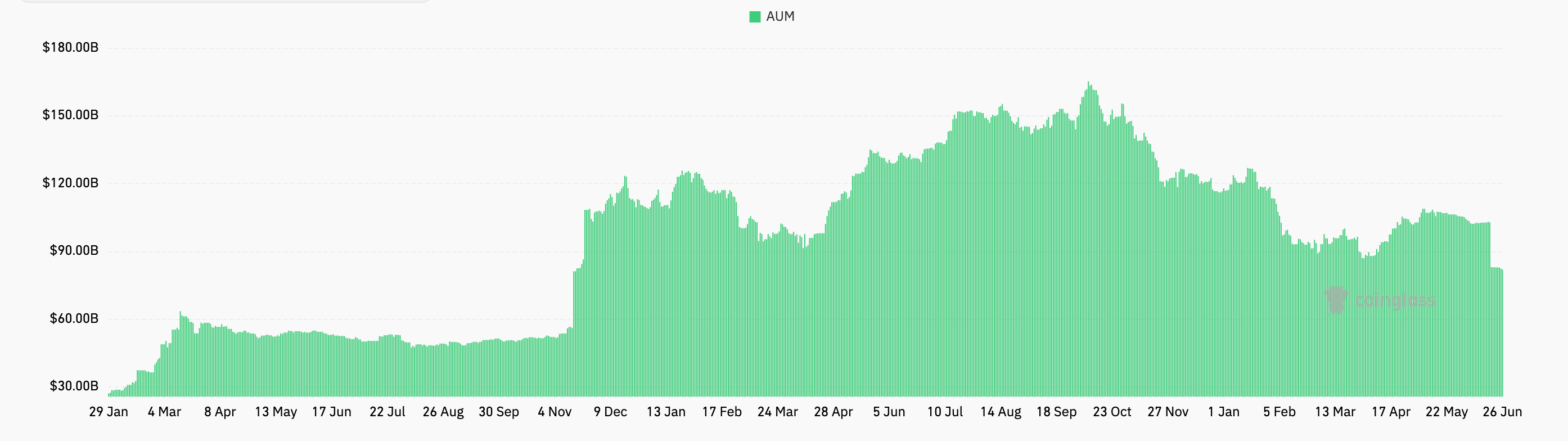

The damage to the products themselves is still significant. Total assets under management fell from above $104 billion to around $80 billion over this period, and cumulative net inflows since launch slid from a peak near $63 billion last October to about $53.4 billion now.

To put it another way, a full year's worth of accumulated capital thinned out in a matter of weeks.

When you ask what's actually pulling the money out, the answer looks a lot more like ordinary portfolio housekeeping than some grand stand on Bitcoin itself.

Marion Laboure at Deutsche Bank now describes Bitcoin as an institutional risk asset, with ETF allocators and corporate treasuries now the marginal buyers. So when those desks decide to trim risk across the board, Bitcoin gets cut right along with everything else, and lately it's been getting cut hard.

A big part of the competition here is AI, as US technology giants are planning more than $700 billion in AI infrastructure spending for 2026. The SpaceX IPO and the pull of private names like OpenAI and Anthropic have also become a magnet for most of the speculative dollars that used to flow toward crypto.

If you look at where these sellers actually bought in, this looks exactly like capitulation. VanEck's on-chain work shows realized losses jumping 78% month over month to $714 million, with the realized-profit-to-loss ratio collapsing all the way to 0.27 from 1.11, and the bulk of those sellers had bought somewhere between $55,000 and $68,000, which means they're locking in losses right near the floor of their own range.

CryptoSlate flagged the early version of this same setup back in May, when fresh redemptions exposed BTC to Wall Street's most crowded trade. Even Strategy got in on the trimming, selling 32 BTC to cover dividend costs in its first net sale since 2022, though, to be fair, the company is still a heavy net accumulator.

Put it all together, and what you've got is coins moving out of the newest, most rattled hands and into the steadiest ones, which is more or less how the ownership base tends to reset near the end of a drawdown.

Why the price keeps sliding even as the strongest hands hold

You'd assume that a market where long-term holders own a record share of the supply would have less Bitcoin available to sell, and that's true. However, it still hasn't managed to put a floor under the price, and the reason is that supply and demand are two separate forces. Right now, demand is the one calling the shots.

Bitcoin trades only on what buyers are willing to pay, and right now, those buyers have gone quiet. Spot volumes have thinned out, on-chain activity has cooled off, and ETF trading volumes have fallen back to levels we last saw during earlier consolidation phases, so while a shrinking float can certainly hold a price steady, it can't lift it on its own without fresh demand to meet it.

The creations that carried Bitcoin all the way through 2025 aren't flowing into the funds anymore, a concern CryptoSlate raised back in March when it asked who buys Bitcoin after five straight weeks of ETF outflows. That demand began to crack in May, when ETF flows absorbed their first real macro shock in seven weeks.

That said, the $6 billion that left is still a single-digit slice of the $53 billion these funds are sitting on. CryptoSlate has previously made the case that headline outflow figures tend to overstate how much spot Bitcoin is actually changing hands.

Long-term holder flows are ten times ETF flows, and those holders are still net accumulating right through the weakness, so, on that measure, the whole sell-off looks more cyclical than structural. BlackRock has made its own version of this argument, treating much of the redemption activity as product rotation within client portfolios rather than as anyone walking away from the asset.

Nonetheless, it still looks rough in the near term. May's inflation data landed hot on Thursday, with headline PCE climbing to 4.1% year over year, its highest reading since 2023, and Bitcoin's reaction was instant: it dropped toward $58,000, dragging more than $1.2 billion in leveraged long positions across the crypto market down with it.

Wednesday alone saw another $469 million leave the funds, their biggest single-day exit since early June, which keeps them on track for a seventh straight negative week. On top of all that, a $10.6 billion Deribit options expiry cleared on Friday, with around 80% of the open interest sitting out of the money and traders bunched around a $60,000 put and an $80,000 call, which put all of that positioning right on top of the level Bitcoin is trying to defend.

And the macro backdrop is offering very little cover, because Kevin Warsh's Fed has already dropped its easing language and nudged its year-end inflation forecast higher, with the market now pricing the odds of a December rate hike somewhere around 77%.

So the divide just keeps hardening. The allocators who came in for clean, regulated, convenient exposure are finding out the hard way that the convenience never actually stripped out the volatility, and they're walking right back out at a loss. The holders who've watched this same sequence play out a few times already are doing what they've always done at the lows: waiting it out.

Wall Street finally owns Bitcoin, and the first real lesson it gave them was a measurement of how much of it these new owners could carry through a proper drawdown. For a meaningful chunk of them, the honest answer turned out to be quite a bit less than they'd signed up for.

The post Did $6B in ETF outflows just mark Bitcoin’s first Wall Street capitulation? appeared first on CryptoSlate.

{kind=link}