Modern systematic trading traces its roots not to code, but to agricultural markets. In the 19th century, exchanges like the Chicago Board of Trade enabled farmers and merchants to hedge price risk through standardized futures contracts. These early markets were dominated by commercial participants—producers and buyers managing uncertainty. Over time, however, speculators entered the market, providing liquidity and transforming price into a function not just of supply and demand, but of expectations and positioning. This shift marked the beginning of financial markets as we understand them today.

The next major evolution came with the introduction of systematic trading. In 1949, Richard Donchian launched one of the first managed futures programs, pioneering a rules-based approach centered on trend following. His philosophy—buy strength, sell weakness, and diversify across markets—replaced intuition with discipline. This was a foundational moment: trading could now be approached as a repeatable system, not a series of discretionary decisions. The concept of “managed futures” was born, laying the groundwork for what would later become the CTA industry.

As futures markets expanded, regulation became essential to ensure transparency and stability. Early legislation such as the Grain Futures Act of 1922 and the Commodity Exchange Act of 1936 established federal oversight of futures trading, aiming to prevent manipulation and standardize exchange practices. These laws laid the groundwork for modern derivatives regulation, recognizing that as markets grew, so did the need for structured governance. They marked the transition from loosely organized trading environments to regulated financial systems.

This framework was solidified in 1974 with the creation of the Commodity Futures Trading Commission (CFTC), which formally defined Commodity Trading Advisors (CTAs) and introduced registration, disclosure, and compliance requirements. Over time, regulation evolved alongside the industry—adapting to electronic trading, global markets, and increasingly complex financial instruments. What began as oversight for agricultural contracts expanded into a comprehensive regulatory structure supporting a multi-trillion-dollar derivatives ecosystem.

Today, markets operate in a fundamentally different environment. Trading in traditional financial markets is nearly continuous—23 hours a day, five days a week—across global futures exchanges. Physical trading pits have been replaced by electronic order books, where transactions occur in milliseconds. Execution is no longer manual but driven by servers housed in data centers, often colocated near exchanges to minimize latency. Speed, connectivity, and infrastructure have become as important as strategy itself.

At the core of this transformation are algorithms. Modern CTA firms and quantitative funds deploy automated systems that analyze price, volatility, and correlations across hundreds of markets simultaneously. These systems do not predict in the traditional sense—they react systematically to changing conditions, scaling positions and adjusting risk in real time. Markets today are shaped by a constant interaction between human intent and machine execution, where price is increasingly the output of code, data, and global liquidity flows rather than individual decisions alone.

Market Structure, First Movers, and Systematic Flows

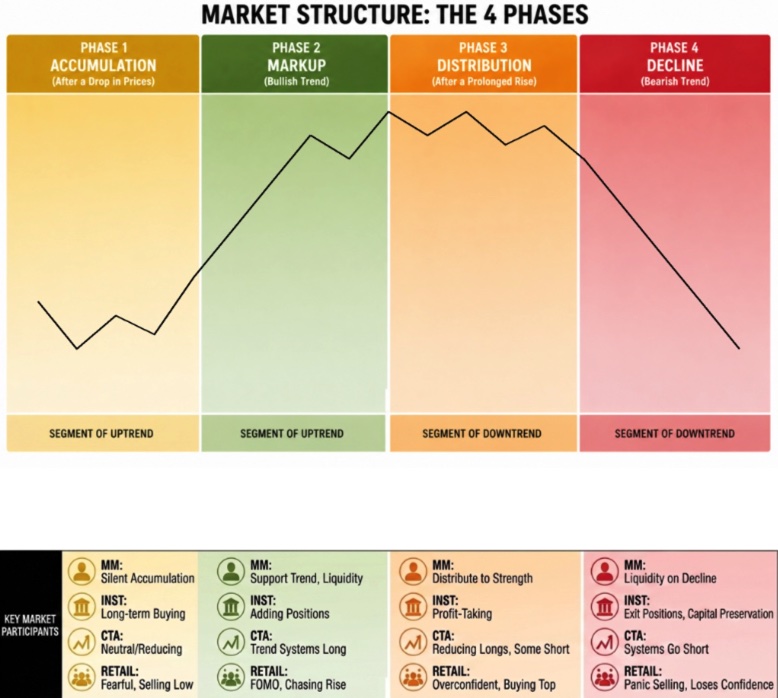

Modern markets are not driven by a single participant, but by layers of activity where different parties enter at different times. Understanding price movement requires looking beyond charts and recognizing how liquidity and participation shift across market structure. A widely used framework, popularized by Brian Shannon, originally proposed by Richard D. Wyckoff, divides markets into four stages: accumulation, markup, distribution, and decline. These stages are not simply visual patterns—they represent transitions in who controls liquidity and how capital flows through the system.

The accumulation phase is where trends begin, but in a quiet and often misleading way. Price typically moves sideways, volatility is low, and breakouts frequently fail. Larger participants begin positioning without drawing attention as market makers balance inventory, institutional traders selectively enter positions, and early capital absorbs selling pressure. Initial movers include market makers and dealers such as JPMorgan Chase and Goldman Sachs, who adjust bids and offers based on inventory needs, as well as informed institutional traders like Bridgewater Associates that act on macro insight, positioning, or information before it becomes widely known. High-frequency trading firms such as Citadel Securities also detect micro-imbalances and test direction, while liquidity seekers target stop levels in thin markets. Together, these participants create the first directional move, which is often exploratory rather than conviction-driven.

Once price begins to shift, stops are triggered, breakout traders enter, and systematic flows begin to engage. This is where the market transitions into markup, the phase where trends become visible through higher highs and higher lows as demand overtakes supply. Participation expands rapidly as momentum traders, breakout strategies, and CTA funds begin buying into strength. CTA firms such as Man Group, Dunn Capital, and Transtrend manage hundreds of billions using leveraged futures, systematic execution, and similar trend-following models. Because they often operate from comparable signals, they tend to buy and sell at the same time, creating powerful feedback loops where rising prices trigger more buying and falling prices trigger more selling. Importantly, CTAs do not usually start the move—they react to it and amplify it.

Their influence becomes clearer when viewed across time horizons. Some CTA programs trade short-term signals lasting days or weeks, while others operate across months. As trends develop, these funds move through a positioning cycle: neutral, initial buying, full long exposure, gradual reduction, and eventually a flip to short if the trend reverses. Large institutions such as Goldman Sachs track these flows using models based on price levels, volatility, and positioning to estimate where billions of dollars of systematic capital may enter or exit. These are not predictions of direction, but maps of potential liquidity flows.

After a sustained uptrend, the market enters distribution. Price begins moving sideways again, but this time at elevated levels. Early participants start exiting positions into strength while late buyers continue chasing the trend, creating failed breakouts and weakening momentum. Although price may still appear strong, underlying demand is fading and the structure becomes fragile. CTAs are often still long during this phase, but the pool of new buyers is shrinking, leaving the market vulnerable to reversal.

When supply finally overwhelms demand, the market moves into decline. Price breaks lower with lower highs and lower lows, stop losses trigger, leveraged positions unwind, and CTA systems begin flipping from long to short. This creates cascading selling pressure where one wave of liquidation leads to another. Unlike the markup phase, which builds gradually, decline is often faster and more violent because forced selling replaces patient accumulation. CTA sell programs accelerate the downside, turning weakness into sharp market dislocations.

The transitions between these stages reveal the deeper structure of markets. The shift from accumulation to markup begins with initial movers, is confirmed by broader participation, and is amplified by systematic flows. The move from markup to distribution occurs when momentum slows and informed participants begin exiting. The final shift into decline is driven by breakdowns that trigger stops, systematic selling, and panic. These transitions are not random—they reflect changes in who controls liquidity at each moment.

Ultimately, market structure is not about recognizing patterns, but about understanding participation. Accumulation is dominated by early positioning, markup by momentum and systematic flows, distribution by the exit of informed participants, and decline by forced selling and risk reduction. Most traders fail because they focus only on price, buying into weakening trends and selling into early accumulation. In reality, markets are driven by the continuous transfer of risk between participants, where price is simply the visible outcome of deeper forces.

On-Chain Markets and the Rise of a New Market Intelligence

On-chain markets aren’t theoretical anymore—they’re already live and actively shaping behavior. The real shift isn’t just infrastructure, it’s visibility combined with personal sovereignty. In traditional finance, participants infer what’s happening through delayed, partial data controlled by centralized institutions. Access to information is gated, and users often surrender privacy and ownership just to participate. On-chain, the underlying mechanics are exposed: wallet flows, liquidity, liquidations, funding, and positioning are visible in real time. The market stops being something you model indirectly and becomes something you can observe as it updates.

At the same time, transparency creates a new requirement: privacy. Open systems should not mean total exposure of the individual. The future of finance depends on balancing system-level transparency with participant-level privacy. Users should be able to see how liquidity moves and how markets function without sacrificing their identity, strategy, or financial autonomy. This is where privacy infrastructure—smart wallets, zero-knowledge systems, and decentralized identity—becomes critical. True decentralization is not just open access, but the ability to participate without relying on permission from centralized intermediaries.

That shift is changing how both crypto-native and traditional players think. Markets are no longer defined by single venues, but by networks of liquidity that operate continuously. Instead of centralized exchanges acting as the core, capital moves across systems, and price reflects that flow. The future market isn’t a place—it’s a state of distributed, always-on liquidity where users maintain ownership of both assets and identity.

This is where the idea of a market superintelligence becomes practical. Even today, most trading frameworks are built around simplified market structure models like accumulation, markup, distribution, and decline. These are powerful because they help traders understand how liquidity shifts across cycles. But they are still human abstractions—ways of compressing a highly complex system into stages we can recognize and act on. The limitation is that participants only find the structures they already know how to look for. A more advanced system wouldn’t start with those assumptions. It would ingest the raw state of the market—price, order flow, funding, liquidations, open interest, cross-exchange activity, liquidity migration, and on-chain positioning—and identify structure directly from the data itself.

Instead of four broad phases, it would likely uncover many small, shifting conditions—micro-states that only exist under specific combinations of liquidity, leverage, and participation. Not simply accumulation or distribution, but highly specific structural environments defined by who controls liquidity in that exact moment. Some of these conditions might only appear briefly, but still carry predictive value and execution advantage. For market participants, this changes how edge is developed. The advantage shifts away from relying only on indicators or directional prediction and toward understanding how liquidity behaves across different structural states. Markets become less about static patterns and more about continuous interaction between liquidity, participation, and flow. In that environment, the edge belongs to participants who can understand and adapt to the deeper structural mechanics shaping the market in real time.

This reframes the problem. This reframes the problem. It’s no longer just about building better models—it’s about building systems that can discover structure on their own and continuously adapt as markets evolve.

On-chain markets make this possible because they provide something traditional systems don’t: complete, real-time data at the structural level. Every transaction, every liquidity change, and every position becomes part of a transparent dataset. That turns the market into more than a place to trade—it becomes a continuous intelligence environment. From there, the direction is clear. The edge shifts from prediction to adaptation. Systems that can process more information, recognize more nuanced states, preserve privacy, and respond faster to changes in liquidity will have a structural advantage.

Markets are moving toward a model that is decentralized in structure, algorithmic in execution, private in ownership, and increasingly intelligent in decision-making. The next step is what happens when those forces fully converge. At that point, you don’t just have better trading systems—you have a new kind of participant altogether. A system that continuously learns from global liquidity, operates across all venues simultaneously, and adapts in real time without relying on human-defined frameworks.

It won’t think in terms of strategies the way funds or traders do. It will operate at the level of structure itself, identifying and acting on patterns that are too complex or too subtle for human cognition. In that sense, it becomes less like a tool and more like an autonomous intelligence embedded within the market, interacting directly with flows rather than reacting to price.

Compared to traditional traders or even large systematic funds, this type of system would exist on a different level—not just faster or more efficient, but fundamentally more capable in how it understands, protects, and navigates markets. As on-chain transparency, privacy infrastructure, algorithmic execution, and data availability continue to expand, the emergence of this kind of intelligence is not a distant concept, but a natural extension of where markets are already heading.

Markets as Living Systems

Across every phase of evolution—from agricultural futures to CTAs, from electronic trading to on-chain liquidity—the underlying pattern has remained the same: markets are not random, they are structured systems driven by participation, liquidity, and flow. What has changed is our ability to see and interact with that structure.

Traditional markets abstracted reality. Participants relied on models to estimate positioning, infer intent, and approximate liquidity. On-chain markets remove that layer. They expose the system directly—turning markets into something closer to a living, observable network, where capital moves, adapts, and rebalances in real time.

This shift reframes everything. Market structure is no longer just a framework for analysis; it becomes a measurable, evolving state. Order flow is no longer hidden; it is visible. Participation is no longer inferred; it is tracked. As a result, the edge moves away from prediction and toward understanding and interaction with the system itself.

At the same time, the rise of systematic trading showed that markets can be influenced—and amplified—by rule-based participants operating at scale. On-chain markets take that one step further by providing the data foundation for systems that can learn, adapt, and evolve continuously. This is where the convergence happens: traditional finance, decentralized systems, and machine intelligence all moving toward the same endpoint.

That endpoint is a market defined by transparency, automation, adaptive intelligence, and increasingly, privacy-preserving infrastructure that allows users to maintain sovereignty while participating in open financial networks. Not just faster execution or better models, but a system where participants—human and machine—interact directly with the underlying structure of liquidity.The implication is clear: the future of markets will not be dominated by those who simply analyze price, but by those who understand how markets are built, how liquidity flows, and how participation shifts across time. Because in the end, price is not the driver—it is the result.

And as markets continue to evolve into open, data-rich environments, the advantage will belong to those who can operate at that deeper level—where structure, flow, privacy, and intelligence converge into a single, unified system.

The post Market Structure Across Eras: From CTA Trading to On-Chain Liquidity and a New Market Intelligence appeared first on Cryptonews.

{kind=link}