Bitcoin price has hit $70,000 after Strategy, the world's largest publicly traded corporate holder of the top crypto, sold a portion of its BTC treasury for the first time since 2022.

Data from CryptoSlate showed that BTC's price dropped 4% on the news to as low as $69,690 before recovering to $70,120 as of press time. This is its lowest price level in six weeks.

This price movement came as Strategy revealed on June 1 that it sold 32 Bitcoin between May 26 and May 31. The sale generated roughly $2.5 million at an average execution price of $77,135.

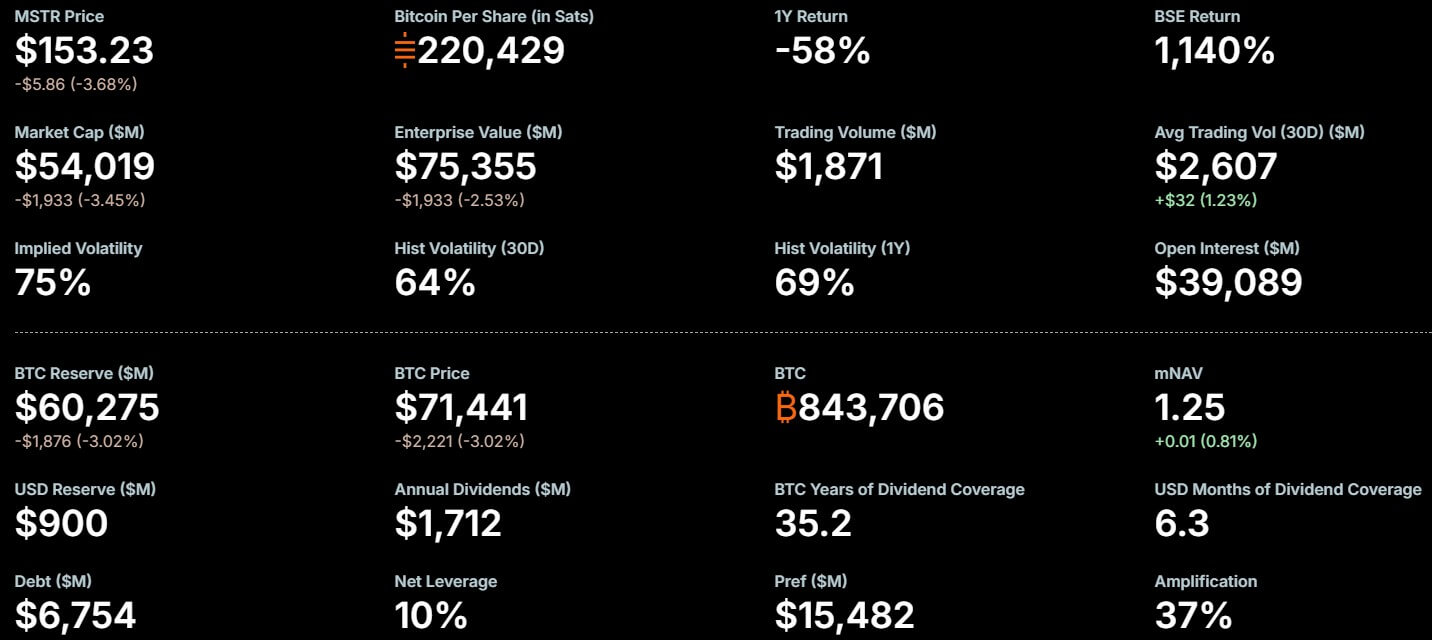

The digital asset sale represents a microscopic 0.0038% of its total holdings against a total corporate stockpile of 843,706 Bitcoin, acquired at an average price of $75,699.

Market observers quickly highlighted the significance of Strategy's decision to sell as a formal departure from the founder Michael Saylor's long-standing doctrine of absolute retention. CNBC's Mad Money host Jim Cramer said:

“Strategy (Micro) sells Bitcoin, $2.5 million. May have to reevaluate pro-bitcoin stance given how much Strategy has propped it up. Key trampoline for years. Some say manipulation. I think that's too strong.”

More importantly, the sale brings an underlying structural risk into sharp relief as Strategy is increasingly relying on a volatile asset to fund fixed, dollar-denominated corporate liabilities.

STRC pulls Strategy deeper into credit markets

According to the filing, Strategy said that it sold its BTC holdings “to fund distributions on preferred stock.”

Over the past year, Strategy has introduced several publicly traded perpetual preferred stocks, including STRK, STRC, STRF, and STRD, to provide fixed-income returns alongside its Bitcoin treasury operations.

The most popular of them is STRC, which is a perpetual preferred stock introduced in July 2025 under the nickname Stretch.

Related Reading

Related Reading

Strategy’s STRC hits record trading volume after massive $1B Bitcoin purchase as market cap doubles since Friday

STRC lets Strategy buy 13,000+ BTC with almost no price swing — now analysts are warning about what happens if the music stops. Apr 14, 2026 · Oluwapelumi Adejumo

In recent months, security has been central to Saylor's effort to turn the company's Bitcoin holdings from a passive reserve into a financing platform that can attract investors seeking yield rather than direct exposure to the token.

Saylor has said Strategy wants STRC to become one of the leading credit instruments in global markets, a goal that depends on keeping the product stable enough to function more like an income vehicle than a volatile crypto-linked equity.

STRC pays monthly cash distributions and currently carries an annualized dividend rate of 11.5%, a level Strategy has held for four consecutive months. The rate is reviewed monthly and can be adjusted to help keep the shares trading close to their $100 par value.

That price anchor is important to the company's broader funding strategy.

When STRC remains near par, Strategy can issue additional shares through its at-the-market program on more favorable terms, thereby raising capital to buy more Bitcoin, meet dividend obligations, and manage liabilities.

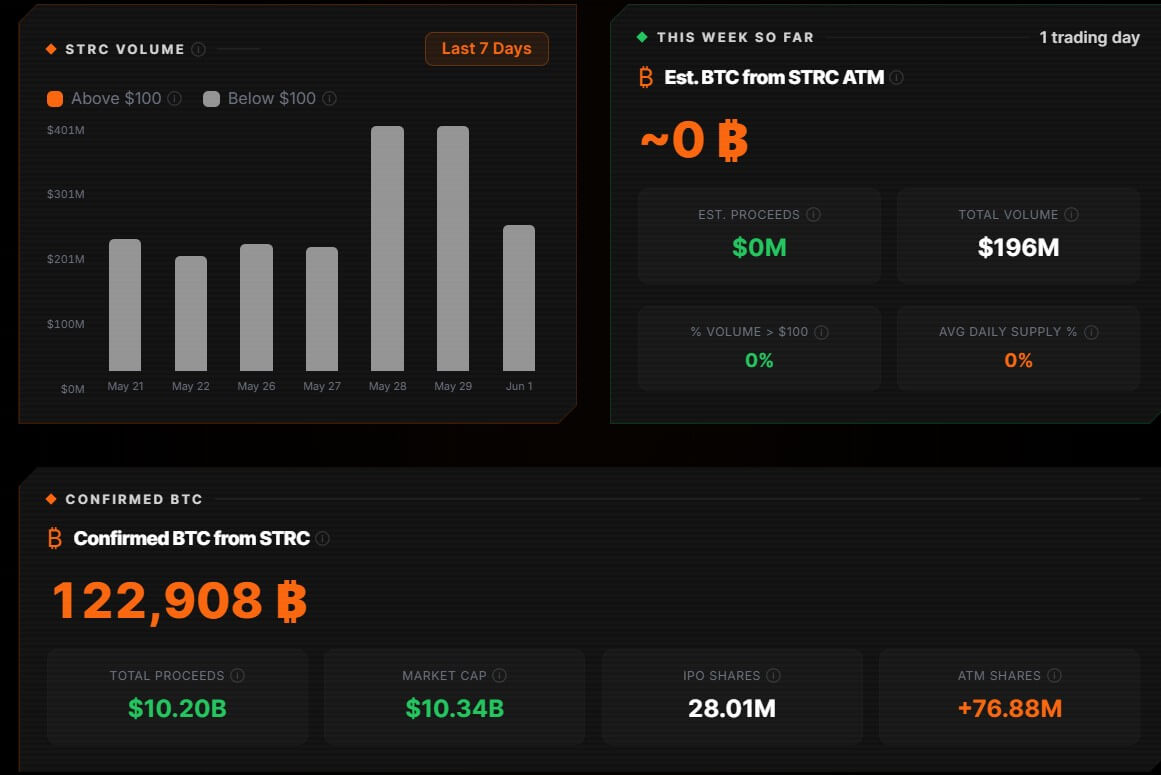

The product, however, has shown some strain recently. STRC has not traded at par since mid-May and fell as low as $97.11 last week before recovering to about $99.10. Still, the product has funded the purchase of more than 122,000 BTC.

Meanwhile, the shares may move closer to $100 ahead of the June 15 ex-dividend date, when investors must own the stock to receive the next payout.

This trading pattern has focused attention on the mechanics behind Strategy's new model.

STRC works best when investor demand keeps the security close to par. If that support weakens, the company may have to rely more heavily on higher yields, equity issuance, or its Bitcoin treasury to keep the structure running smoothly.

The harder question is not whether Bitcoin can be sold

Strategy and its supporters have presented the 32-Bitcoin sale as a way to show that its treasury is not locked away from the market.

The company argues that it can sell when doing so supports its balance sheet, improves per-share metrics, or helps meet obligations tied to the securities it has issued around its Bitcoin holdings.

However, critics argue that this explanation addresses only part of the concern now forming around the company.

Glenn Cameron, global head of institutional at Onramp Bitcoin, noted that Bitcoin's liquidity has never been the central doubt for institutional investors. The asset trades continuously across global venues and routinely clears tens of billions of dollars in daily volume.

According to him, the more difficult question is whether Strategy can rely on that liquidity during a sustained drawdown, when fixed dollar payments remain due, and other funding channels may be less attractive.

He wrote that the company's model rests partly on the idea that Bitcoin would need to appreciate by only about 2.3% a year to cover an estimated $1.6 billion STRC dividend bill over time.

According to him, the calculation is based on the dividend bill relative to the current notional value of Strategy's Bitcoin holdings. At today's prices, a modest gain in the treasury can appear sufficient to offset the cash cost of the payout.

Dividends, though, are not paid with mark-to-market gains. They require dollars. That distinction becomes more important when the value of the underlying treasury falls.

If Bitcoin's price were cut in half, the same dividend obligation would consume a larger share of the company's asset base.

However, if Strategy continues issuing preferred shares, the cash burden would also grow. A manageable breakeven rate in a rising market can become more demanding when the treasury value contracts and the dividend bill stays fixed.

That is where the 32 Bitcoin sale takes on more significance than its size suggests. The transaction did not test Strategy's ability to sell Bitcoin at scale. It showed how the treasury could be used once cash obligations tied to the preferred-stock structure come due.

A downturn would narrow Strategy's options

In a supportive market, Strategy can draw on several funding channels simultaneously. Common-share issuance can raise cash. Preferred shares can trade close to par. Bitcoin sales can be limited and presented as selective balance-sheet management. A rising Bitcoin price also reinforces the value of the treasury backing the structure.

Those conditions become harder to rely on during a drawdown. A weaker common stock price makes equity issuance more dilutive. A lower STRC price can force the company to offer more yield to restore demand.

Meanwhile, dividend payments must still be made in cash, regardless of where Bitcoin trades.

That is the scenario drawing scrutiny from analysts. If capital markets remain open, Strategy can fund its obligations without leaning heavily on the Bitcoin stack. If market access tightens, the treasury becomes a more visible source of liquidity.

Repeated sales in a falling market would carry their own risks. A lower Bitcoin price would require more coins to meet the same dollar obligation, while each sale could deepen investor concern about whether the preferred-stock structure is beginning to feed on the asset it is meant to support.

Jeff Dorman, chief investment officer at Arca, has argued that the small sale may be preparing investors for larger disposals later.

He has also warned that Strategy's $900 million cash reserve covers only about five months of dividend obligations, leaving the preferred-stock structure more exposed if issuance becomes harder.

Dorman described the setup as a “ticking time bomb,” saying the interests of common shareholders, preferred holders, and Bitcoin investors may not always move together once fixed cash payouts are layered onto a volatile treasury.

Meanwhile, that tension extends beyond Strategy. Public Bitcoin treasury companies are no longer simple holders of a reserve asset.

Once they issue yield-bearing securities and rely on traditional capital markets, they take on obligations to shareholders and capital providers that can complicate a pure hold-through-volatility strategy.

Simon Dixon, a Bitcoin analyst, said investors should recognize that the managers of public treasury companies now operate inside a broader financial structure. He said:

“Those who care about Bitcoin should understand who Adam, Saylor and others running Bitcoin treasury companies ultimately work for now, and adjust their expectations accordingly.”

Strategy has turned Bitcoin into the base layer of a corporate credit strategy. The question now is how that structure behaves if the market stops supplying the conditions that made it work: rising Bitcoin prices, steady investor demand, and open access to new capital.

The post Strategy sold 32 BTC to pay dividends – But the real risk is what happens if it has to sell more Bitcoin appeared first on CryptoSlate.

{kind=link}